Elevate your wealth management with our platform's no-code configurability.

Empower your wealth management practice with comprehensive integration capabilities.

Choose the modules your business needs, and fit them into your existing ecosystem.

Design the wealth management solution that’s right for your firm.

Personalize client onboarding using digital tools to meet client and advisor needs.

Customize your client portal in moments—no coding needed.

Stay ahead of requirements with advanced management tools.

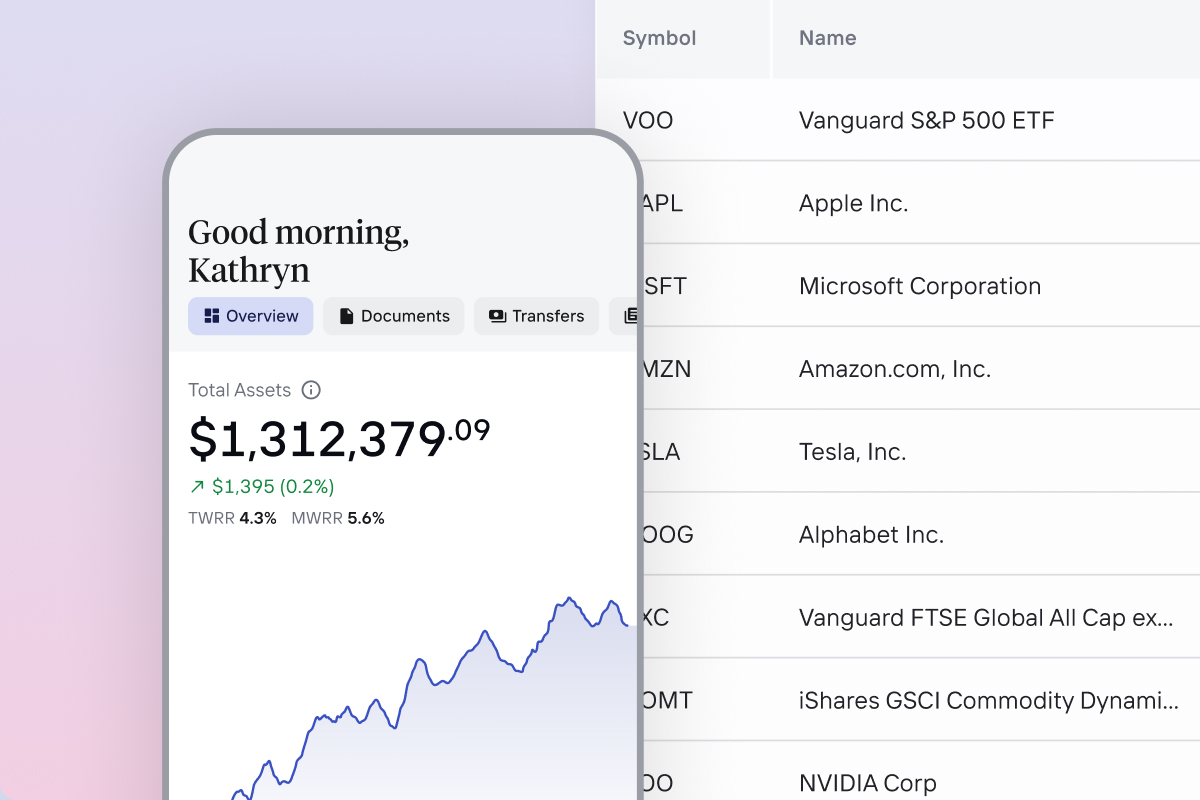

Elevate your financial oversight with a clear view of client portfolios.

Build portfolios, manage client investments, and automate processes.

Customize fees by organization, relationship, and accounts.

Power growth with intelligent workflows that adapt to your business.

Modernize your institution's approach to wealth management.

Empower advisors to spend more time engaging with clients.

Launch your wealth program with a platform that makes it easy.

Streamline operations with a platform that integrates seamlessly.

Seamlessly integrate investment options into your current offering.

Stay ahead of industry demands with a platform built to scale and evolve.

Launch new lines of business within your existing ecosystem.

An interface that empowers advisors to manage clients, portfolios, and workflows.

A digital experience that gives clients visibility into their goals and portfolios.

Tools for operations, compliance, and supervision to support scale and efficiency.

Learn about our mission, values, leadership team, and more.

Discover our latest news, achievements, and industry recognitions.

Get expert insights on modern wealth management.

Interested in joining our talented team? Explore open positions and apply today.

FAQs, support, and more.

Necessary for the site to function. Always On.

These items are used to deliver advertising that is more relevant to you and your interests. They may also be used to limit the number of times you see an advertisement and measure the effectiveness of advertising campaigns. Advertising networks usually place them with the website operator’s permission.

These items allow the website to remember choices you make (such as your user name, language, or the region you are in) and provide enhanced, more personal features. For example, a website may provide you with local weather reports or traffic news by storing data about your current location.

These items help the website operator understand how its website performs, how visitors interact with the site, and whether there may be technical issues. This storage type usually doesn’t collect information that identifies a visitor.