OneVest Pulse: The Live Activity Stream Where Conversation Becomes Command

Fast-growing wealth management firms require solutions that can keep pace with the shifting operational needs of wealth management firms and their advisors. As firms scale, the way teams collaborate becomes a critical factor in their success. When we look closely at the challenges that slow firms down, fragmented collaboration and repetitive manual work are consistently the biggest hurdles.

Advisors and operations teams often find that email is the ultimate "swivel-chair" tool, it is where they live, yet it is disconnected from their core systems. Constantly toggling between an inbox and a wealth platform to move a single task forward creates a drag on productivity.

Bridging the Gap Between Chat and Execution

To solve the friction of "operational drag," firms need more than just another internal chat tool; they require a unified interface where communication and data exist in the same space. The ideal solution is a system that bridges the gap between high-level advisor conversations and back-office execution. It should allow team members to communicate, assign tasks, and trigger complex workflows without ever losing the context of the client or the account they are discussing. By centralizing these interactions, a firm can ensure that every decision is logged, every handoff is seamless, and every team member, from the advisor to the home office, is looking at a single source of truth.

OneVest Pulse was created as a direct response to these specific challenges. It serves as a live command layer that integrates real-time messaging, team collaboration, and agentic execution into a single, context-aware stream.

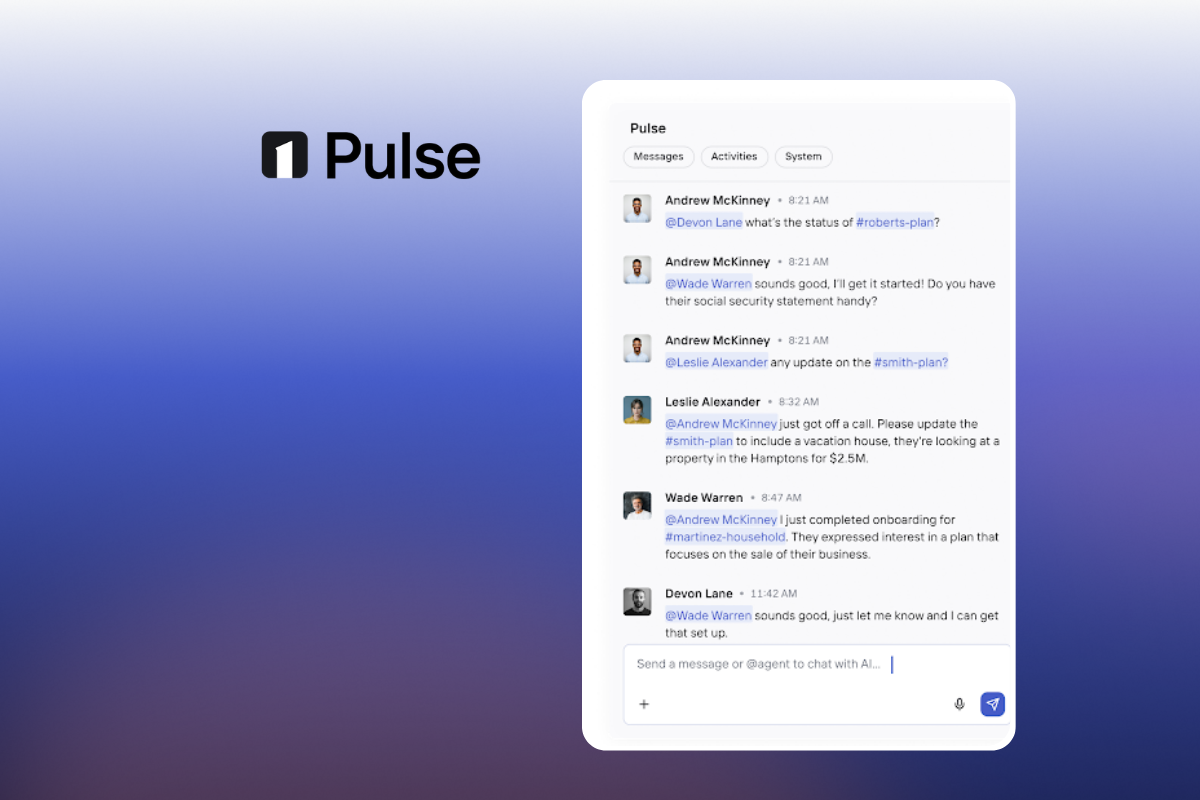

Pulse runs alongside the main content of every workspace, whether you are viewing a client, an opportunity, or a specific case. It provides a chronological, audit-ready history of every action taken within the firm, finally enabling advisors and their teams to communicate and execute in one place.

Why Pulse is the Strategic Link in Your Tech Stack

1. Unified Integration with Microsoft Teams & Slack

The biggest barrier to institutional speed is the disconnect between communication and execution. OneVest Pulse bridges this gap:

Centralized Visibility: Pulse syncs your team chats and assigned tasks directly with Slack and Microsoft Teams so updates exist in both places. This ensures that whether a task is assigned in the platform or discussed in a channel, the entire team stays aligned in real-time.

Bi-Directional AI Command: Beyond simple notifications, you can chat directly with the OneVest agent within Slack or Teams. This allows you to create tasks, trigger cases, and execute workflows using natural language from your mobile device or desktop without ever leaving your primary communication tool.

2. Context-Aware Messaging & Smart Tagging

Unlike a standard chat app, every entry in Pulse is inherently linked to a specific record.

Smart Mentions (@): Tag specific users, teams, or the AI Agent to bring them into a workflow.

Email Synchronization: On client pages, Pulse syncs emails from connected inboxes, placing client communications directly alongside internal notes and system events.

Secure Client-to-Advisor Chat: Pulse serves as the bridge between the advisor team and the client. Through secure messaging, advisors and operations can communicate directly with clients via the client app. These conversations flow into the same Pulse stream, keeping all client-facing and internal dialogue in one organized, context-rich location. In a world of increasing financial fraud, this encrypted channel provides clients with the peace of mind that they are always interacting within a verified, protected environment rather than over vulnerable email.

3. Ask Anything, Execute Anywhere

Pulse introduces a conversational interface for firm-wide data. Using the + Quick Actions menu or natural language chat, teams can:

Log Activities: Enter recorded calls, meetings, or notes as activities for the rest of the team to see.

Execute: Launch new Tasks or Opportunities that are automatically linked to the current client or account. You can ask Pulse to start workflows like onboarding, account opening or money movement.

AI Enrichment: Use the AI Enrich action to extract key data from stored emails and attachments, transforming raw text into actionable insights.

Voice-to-Action Commands: Use natural voice language to command and refine tasks on the fly. Simply speak to Pulse to update records or adjust workflows, making it faster to execute and manage operations while on the go.

The Benefits of Unified Team Collaboration

OneVest Pulse serves as a high-speed collaboration hub, enabling seamless chat communication between advisors, operations, and home office teams. By housing these interactions in one place, firms can move away from scattered email threads and siloed spreadsheets.

Centralized Communication: Pulse enables real-time chat between advisors and their support teams, ensuring everyone is aligned on client needs without leaving the platform.

Organization by Context: Because messages and discussions are attached directly to relevant files and records, teams stay organized. You no longer spend time looking for the "latest version" of a document or the status of a request; the context is always right there.

Operational Efficiency: Collaboration happens more efficiently when the data is adjacent to the discussion. Teams can resolve questions and move workflows forward in significantly less time.

Compliance & Audit Readiness: Compliance teams have a full audit trail available at their fingertips. Every internal discussion, file attachment, and system change is logged, making regulatory reviews straightforward and transparent.

From Back-Office Productivity to Front-End Client Results

OneVest Pulse serves as the central hub for the entire firm, housing all communication between advisors, operations, support, and home office teams in one place. By centralizing these chats, firms ensure that every internal stakeholder stays aligned without the need for fragmented email chains.

For Advisors

Advisors can manage their book of business more efficiently by triggering commands via conversation. By interacting with the AI Agent via Slack or Teams, they can pull data or launch workflows while on the move, reducing time spent on administrative data entry and manual follow-ups with support teams.

For Operations & Support Teams

Pulse places operations and support at the center of a streamlined flow. Because the communication with the advisor is housed directly alongside the record, teams have immediate context. With Related Items such as upcoming tasks and open opportunities on display, they no longer have to dig through menus to identify what requires attention.

For the Home Office & Compliance

By consolidating advisor, ops, and support communications into one place, Pulse provides the Home Office with a "Master View" of firm activity. Every action, whether human-driven or AI-driven, is logged in a permanent, read-only audit trail. Compliance teams can filter by System events to see a transparent history of record changes, ensuring the firm remains audit-ready at all times.

Frequently Asked Questions

What is an Agentic Wealth OS?

An Agentic Wealth OS is a comprehensive platform where AI does more than just summarize data. It acts as an agent capable of executing complex workflows, routing approvals, and managing back-office tasks autonomously. OneVest Pulse serves as the interface for this interaction.

How does AI improve wealth management platforms?

AI increases firm capacity by automating repetitive administrative tasks, such as data extraction and meeting logging. In OneVest, the AI Assistant provides context-aware support directly within the Pulse feed to help teams make faster, data-driven decisions.

Why is integration with Slack and Microsoft Teams important for RIAs?

Most wealth management communication happens outside the CRM. By integrating with Slack and Teams, OneVest Pulse ensures that these conversations are captured, compliant, and linked to actual operational tasks.

Can OneVest Pulse help with regulatory compliance?

Yes. Pulse maintains a permanent, read-only audit trail of all system and audit events. This ensures that every record change or approval is logged and traceable, simplifying the reporting process for compliance officers.

How does Context-Awareness work in a wealth platform?

Context-awareness means the system knows exactly which client, account, or task you are discussing. When you post in Pulse on a client’s page, the system automatically links that data, preventing the information silos common in traditional software.

Stop Managing Software. Start Deploying Intelligence.

The future of wealth management is found in the elimination of friction. By integrating with Microsoft Teams and Slack and turning every message into a context-aware command, OneVest Pulse ensures your firm moves as fast as the markets.

Book a Demo Today and see how we’re turning talk into action.