RIA M&A Integration Challenges and How Agentic AI Solves Them

RIA M&A activity has not slowed down. The number of transactions hitting the market each year continues to rise, deal multiples remain competitive, and acquiring firms are under pressure to close faster, integrate faster, and demonstrate growth faster than the cycle before.

What has not kept pace with the deal volume is the integration infrastructure most firms bring to the table after signing.

The challenges of RIA M&A integration are not new, but they are getting worse. Acquiring firms are absorbing practices with incompatible technology stacks, fragmented client data, and advisor teams that operate with habits built around systems that are about to change. The window between deal close and full operational integration is where acquisitions either generate the value they promised or quietly consume it.

Agentic AI is changing what is operationally possible in that window. Not by making integration painless, but by compressing the timeline and reducing the manual coordination burden that has defined post-merger operations for the past decade.

Why Post-Merger Integration Fails Quietly?

Most RIA acquisitions do not fail loudly. The firm does not collapse. The advisors do not all leave on day one. What happens instead is slower and more expensive: the integration takes longer than projected, clients experience service gaps, compliance documentation falls behind, and the advisors who were supposed to drive growth spend the first six to twelve months managing operational friction instead.

The root cause is almost always the same. Post-merger integration is treated as a project with a finish line, a checklist of systems to connect and processes to migrate, rather than as an ongoing operational challenge that requires scalable infrastructure to manage. When a firm closes two or three acquisitions in a single year, as many growth-oriented RIAs are now doing, there is no clean finish line. The integration work is perpetual.

The challenges of RIA M&A integration compound quickly when firms are running multiple integrations simultaneously. Technology workflows built for a single custodian relationship have to accommodate new ones. Compliance oversight programs designed for one firm's practices have to expand to cover advisor teams with different habits, different documentation standards, and different client communication norms. Onboarding processes that work at steady state break under the volume that an acquisition introduces.

The Technology Stack Problem Is Bigger Than It Looks

RIA tech stack modernization is consistently cited as one of the top post-merger priorities and one of the most consistently underestimated challenges. On paper, technology consolidation looks like a finite project. In practice, it is an extended negotiation between operational continuity and the long-term goal of running a unified platform.

The acquired firm's advisors built their practices around the tools they have. Their CRM contains years of client interaction history. Their portfolio management system has customized model structures, fee schedules, and reporting configurations that took time to build. Moving those advisors onto a new platform is not just a technical migration. It is a behavioral change management challenge wrapped inside a technical one.

The typical approach is to run parallel systems through the transition period, maintaining the acquired firm's existing infrastructure while building toward consolidation. This limits disruption but creates its own problems. Compliance oversight has to cover two sets of systems. Client data exists in two environments. Any report that requires a consolidated view of the combined firm requires manual aggregation from multiple sources.

Without RIA tech stack modernization that is designed for integration from the ground up, this parallel-system period stretches. What was projected as a six-month transition becomes eighteen months. The operational drag accumulates, and the growth thesis that justified the acquisition gets deferred.

Technology Is Now a Recruiting Asset, Not Just an Operational One

There is a dimension of the technology conversation that acquiring firms often underweight: advisor teams evaluating a potential home are paying close attention to the platform they will be working on.

These moves are not casual decisions. Advisors making a transition to a new firm are often leaving behind equity, deferred compensation, or other incentives. The bonuses tied to these moves are significant, and so is the career risk. When an advisor team is weighing their options, the quality of the technology they will inherit is a concrete part of the calculus.

A firm with a fragmented, manual-heavy operational environment is asking advisors to trade a known platform for one that will slow them down. A firm with modern, integrated technology infrastructure is offering something different: the ability to spend more time on client relationships and less time managing operational noise. For high-producing advisor teams with real leverage in the negotiation, that distinction can be the deciding factor.

This means that RIA tech stack modernization is not just about internal efficiency. It is a competitive differentiator in the market for advisor talent. Firms that have invested in their operational platform are not just running more efficiently. They are winning deals that firms with legacy infrastructure are losing, because the best advisor teams have choices and they choose environments where they can produce.

Advisor Onboarding Is Where Value Leaks Out

The deal was built on advisor productivity. The acquiring firm modeled what those advisors would generate once they were operating on the combined platform with access to broader capabilities, better technology, and more scalable operations. That model only works if the transition does not break what made those advisors productive in the first place.

Advisor onboarding in the context of an acquisition is more complex than standard new-hire onboarding. These advisors are not starting fresh. They are carrying existing client relationships, compliance history, and operational habits that have to be mapped to a new environment. Every client account has to be reviewed and transitioned. Every disclosure has to be updated. Every workflow the advisor uses has to have a functioning equivalent on the new platform before they can operate without disruption.

The manual version of this process is sequential, slow, and heavily dependent on the bandwidth of operations staff who are already managing everything else that comes with post-merger integration. It creates a bottleneck that delays advisor productivity and generates compliance risk when documentation and disclosure updates fall behind the pace of account transfers.

The firms absorbing acquisitions without a structured, technology-supported advisor onboarding process are not just slowing down. They are creating concentrated risk in the first ninety days of every deal, exactly when client retention and advisor satisfaction are most sensitive.

What Agentic AI Changes About the Integration Model?

Agentic AI does not eliminate the complexity of RIA M&A integration. What it does is change how much of that complexity requires manual coordination.

The core value is continuity across multi-step, multi-system processes. Where a traditional workflow requires a coordinator to pull data from the acquired firm's CRM, reconcile it against the acquiring firm's records, identify gaps, and route action items to the right people, an agentic system moves through those steps continuously and surfaces the exceptions that require human attention without someone managing the process end to end.

In practice, this looks like a system that monitors advisor onboarding status across every account in the acquired book, surfaces missing documentation and disclosure gaps in real time, tracks completion against defined timelines, and routes unresolved items to the appropriate reviewer before they become compliance findings. The operations staff are not coordinating the process manually. They are managing a prioritized queue of items that actually require judgment.

The same logic applies to compliance oversight across a newly expanded firm. An agentic compliance layer can extend supervisory monitoring to advisor teams from the acquired firm from the moment they are onboarded to the platform, tracking account activity, document status, and servicing exceptions without requiring the compliance team to build out new manual workflows for each acquisition.

This capability matters most for firms running multiple acquisitions. Each new deal does not require building a new integration process from scratch. The infrastructure scales. The marginal cost of the next acquisition, measured in operational overhead and compliance exposure, decreases rather than increasing proportionally with deal volume.

The Compliance Dimension of Integration Is Underestimated

The challenges of RIA M&A integration have a compliance dimension that deal teams often underweight during diligence and then confront at scale during integration.

The acquired firm operated under its own compliance program. It may have had different documentation standards, different supervisory procedures, and different policies around areas like outside business activities, marketing, or fee disclosures. On day one after close, those advisors are operating under the acquiring firm's compliance obligations, but the documentation infrastructure that supports oversight of their activity has to be built.

Regulators do not grant grace periods for post-merger integration. An SEC examination that occurs twelve months after a transaction closes will expect to see supervisory documentation that covers the full period of the combined firm's operations, including the accounts and advisors absorbed through the acquisition. If those records exist in a legacy system that was not fully integrated, or if they were maintained through manual processes that created gaps, the examination exposure is real.

The firms managing this well are the ones that deploy compliance infrastructure before the deal closes, not after. Due diligence surfaces the compliance profile of the target. The integration plan defines how supervisory monitoring will extend to the acquired team from day one. The technology makes that extension operationally sustainable.

Building an Integration Infrastructure That Scales

The distinction that separates firms that integrate well from those that struggle is not the size of the integration team. It is whether the firm has built integration infrastructure or is assembling integration process from scratch with each deal.

Infrastructure means that the key workflows, including advisor onboarding, compliance oversight expansion, client account migration, and document and disclosure tracking, have defined processes supported by technology that can be activated for a new acquisition without rebuilding from scratch. It means that the firm can run multiple integrations simultaneously without each one competing for the same pool of operational bandwidth.

For firms running the integration as a manual project, each acquisition is roughly as hard as the last one. The team learns from experience, but the underlying process remains labor-intensive, and the compliance exposure in the transition period remains largely unchanged.

For firms operating on a platform designed to support growth through acquisition, the second deal is easier than the first. The third is easier than the second. The infrastructure compounds in the same direction as the growth thesis.

What to Look for in a Platform Built for Acquisition-Driven Growth?

Not all wealth management platforms handle the operational demands of acquisition-driven growth equally. Evaluating technology through the lens of integration capability rather than steady-state functionality changes the criteria considerably.

Integration depth matters more than feature breadth. A platform that connects deeply with the custodians and data sources the acquired firm relies on is worth more than one with an impressive feature list that requires manual data bridges to function. The first question is always whether the platform can absorb the acquired firm's data environment without a prolonged parallel-systems period.

Onboarding workflow automation is a practical differentiator. Platforms that support structured advisor onboarding, tracking completion status, surfacing gaps, and routing exceptions, reduce the manual coordination burden that slows every transition.

Compliance scalability is non-negotiable for firms planning serial acquisitions. Every deal that closes increases the compliance surface area. A compliance oversight model that requires adding headcount proportionally to acquisition volume is a model with a ceiling. Firms that want to grow through acquisition without proportional compliance infrastructure growth need a platform whose supervisory tools extend automatically as the firm expands.

Frequently Asked Questions

What are the most common reasons RIA acquisitions underperform their growth projections?

The most frequent cause is post-merger integration taking longer and consuming more operational resources than projected. Advisor productivity is deferred while teams manage technology transitions. Compliance documentation falls behind account transfers. Client service gaps during the transition period create retention risk. These are operational failures, not strategic ones, and they are preventable with the right infrastructure.

How long does advisor onboarding typically take during an RIA acquisition?

Without structured, technology-supported workflows, full onboarding of an acquired advisor team, including account transfers, disclosure updates, and compliance documentation, typically takes three to six months per deal. Firms running multiple acquisitions simultaneously often find these timelines extending further as operations resources are pulled in multiple directions. Automated onboarding workflows can reduce this significantly by eliminating the manual coordination bottleneck.

What role does technology play in RIA due diligence?

Technology assessment should be a standard component of acquisition due diligence, not an afterthought. The acquired firm's tech stack determines the complexity and cost of integration. Evaluating CRM, portfolio management, and custodian relationships before close allows the acquiring firm to build a realistic integration timeline and cost model, and to identify whether its own platform can absorb the acquired firm's environment without an extended parallel-systems period.

Does the quality of an acquiring firm's technology affect its ability to recruit advisor teams?

It does, and more than many firms realize. Advisor teams evaluating a move are making a high-stakes decision. The compensation tied to these transitions is significant, and advisors with strong books have real options. A modern, integrated operational platform is a tangible differentiator in those conversations. Firms with legacy or fragmented technology are asking advisors to accept an operational downgrade. Firms that have invested in their platform are offering advisors a path to doing more with less friction.

How does OneVest support firms growing through acquisition?

OneVest provides an integrated operational platform built to scale with acquisition-driven growth. Advisor onboarding workflows, compliance supervisory monitoring, and client account management extend to acquired teams from day one, without requiring firms to rebuild integration processes from scratch with each deal. The platform's agentic AI layer continuously monitors activity across the combined firm, surfaces exceptions for human review, and maintains a complete audit trail, allowing compliance and operations teams to manage a growing advisor population without proportional headcount increases. [LINK: learn more about OneVest for acquisition-driven RIAs → OneVest platform overview]

Conclusion and Next Steps

The challenges of RIA M&A integration are not going to get simpler. Deal volume is not declining, advisor teams are scrutinizing technology more carefully than ever, and regulatory expectations for supervisory documentation do not pause for transition periods. Firms growing through acquisition are operating in an environment where each deal adds complexity that has to be absorbed, and where the gap between firms with modern integration infrastructure and those still managing the process manually is widening with every transaction.

The firms executing acquisition-driven growth effectively right now are not necessarily the ones with the largest integration teams. They are the ones that have built scalable operational infrastructure underneath their advisors, infrastructure that extends onboarding workflows, compliance monitoring, and client account management to each new team without rebuilding from scratch. That infrastructure is what allows the third acquisition to be easier than the second and the fifth to be easier than the third.

Every advisor team a firm absorbs, every custodian relationship it adds, every market it enters through acquisition increases the operational surface area that has to be managed. That surface area becomes manageable when the firm is operating on a platform designed to scale with it. Without that platform, each expansion creates new exposure and defers the productivity the deal model was built on.

The next step for any M&A-focused RIA principal or growth officer is practical. Map your current integration workflow from deal close to full advisor productivity. Identify where manual coordination is creating delays, where compliance documentation is falling behind account transfers, and where your current technology would break under the volume of two or three simultaneous integrations. Then evaluate whether your operational platform can support the pace of growth your strategy demands.

Modern integration infrastructure is not about removing the judgment that makes acquisitions work. It is about giving that judgment the operational support it needs to function at scale and at speed.

Ready to build an acquisition infrastructure that scales? Join leading RIA firms already using OneVest to integrate advisor teams, automate onboarding workflows, and maintain exam-ready compliance documentation across every deal. Explore OneVest.

Keep Reading

Blog

BlogHow to Onboard New Advisors Faster: The 2026 Blueprint for Scalable RIA Growth

There's a moment every growing RIA knows well. You've made the hire. The advisor is talented, the fit is right, and the opportunity is real. Then the clock starts, and so does the cost. Every week an advisor isn't fully productive is revenue your firm hasn't earned. Every process they have to learn the hard way, every data entry task left to them to figure out, every system they access through a different login with a different workflow: it compounds. The gap between "hired" and "generating value" is where advisor growth strategies quietly break down. In 2026, that gap is getting harder to ignore. The 2026 T3/Inside Information Software Survey, the largest advisor technology survey in the profession with 2,906 respondents, found that proposal generation and client onboarding tools jumped from 15.84% market penetration in 2025 to 21.45% this year. Firms are investing here. But adoption alone doesn't close the productivity gap. How you structure the onboarding process does. This is a blueprint for RIA ops and HR leaders who want to onboard new advisors faster, with less friction, and in a way that scales as the firm grows. Why Advisor Onboarding Is an Operational Problem, Not an HR One? Most firms treat new advisor onboarding as an orientation function. Get the person their laptop, walk them through the compliance manual, and introduce them to the team. Done. That's not onboarding. That's processing. Real onboarding for an advisor means they can access client data, run a financial plan, generate a compliant proposal, record meeting notes, and hand off action items to operations without help within 30 days. For many RIAs, that timeline is closer to 90 days, and for some it stretches further. The cost isn't just the salary you're paying while productivity ramps. It's the clients who don't get touched while the new advisor finds their footing. It's the referrals that get delayed. It's the experienced advisor who loses two hours a week pulling the new hire through systems they barely understood themselves. This is an operational design problem. And like most operational problems, it has a structural solution. What Slows New Advisors Down? Before you can fix the onboarding timeline, you have to diagnose where it breaks. In most firms, the friction lives in three places. Tech stack fragmentation: The average RIA uses a CRM, a financial planning tool, a portfolio management system, a document processor, a compliance tool, and some form of scheduling software, often none of which talk to each other natively. The 2026 T3 survey found CRM adoption at 91.08% across advisory firms and financial planning software at 83.3%. But most firms are running these as separate tools, each with its own data entry conventions and workflow logic. A new advisor has to learn not just the tools but the firm's workarounds between them. Undocumented tribal knowledge: Every firm has a version of "how we actually do things here" that lives in the heads of senior advisors and ops staff. Prospect intake, client segmentation, meeting prep, post-meeting follow-up: these processes exist, but they aren't written down in a way that translates to a new hire. The new advisor is dependent on interrupting someone who already has a full book of business. Compliance bottlenecks: Before a new advisor can start client-facing work, there's a credentialing and compliance setup process that varies by firm, custodian, and state. When that process is manual, with paper forms, email chains, and PDF attachments, it takes longer than it should and creates gaps in the audit trail that come back up in exams. Each of these friction points is solvable. Not all at once, but in sequence. Step One: Standardize Before You Automate The instinct when onboarding is slow is to add tools. Buy the onboarding software. Subscribe to the AI assistant. Set up the workflow platform. That instinct is wrong, or at least premature. Tools automate processes. If the process isn't defined, the tool just moves chaos faster. Start by documenting what a fully productive advisor actually does in their first 30, 60, and 90 days. What systems do they need access to? In what order? What client-facing activities can they begin immediately, and what require supervisor sign-off? What does "ready to manage a book" mean at your firm, specifically? That documentation becomes the onboarding playbook. It's the single source of truth that lets a new advisor navigate the first 90 days without constant hand-holding, and lets ops leaders identify exactly where delays are occurring when things go wrong. This sounds simple. Most firms haven't done it. Step Two: Audit the Tech Handoff Once the process is documented, map it against the tech stack. For every step in the onboarding playbook, answer: which system handles this, who owns that system's setup, and how long does provisioning take? This audit almost always reveals two things. First, there are more access dependencies than anyone realized: a new advisor can't fully use System B until they're set up in System A, which requires approval from a third party that takes five business days. Second, some steps in the process are entirely manual because no one ever built a better option, even when one exists. It's also worth assessing whether the tools themselves are earning their place. The 2026 T3 survey found that CRM average user satisfaction jumped from 7.21 in 2025 to 7.70 in 2026, the sharpest single-year improvement of any major category. That shift reflects meaningful platform improvements across the market. If your CRM is one a new advisor finds frustrating to learn, that friction is now largely avoidable. This is also where agentic AI starts to change the calculus. An agentic layer sitting across your tech stack can handle provisioning triggers, surface the right data at the right step, and route tasks to the right person automatically. That's not theoretical: it's how the most forward-looking firms are collapsing what used to be a five-step manual handoff into a single configured workflow. The 2026 T3 survey found that AI notetaking tools, a category that barely existed two years ago, are now used by 42.86% of advisory firms. Firms that adopted early aren't using these tools just to capture meeting notes. They're using them to reduce the documentation burden on new advisors who are still learning how the firm expects meetings to be run. That's a meaningful unlock: a new advisor who can walk out of a client meeting with a structured summary, automated action items, and a draft follow-up message isn't behind. They're operating at the same output level as a five-year veteran. Step Three: Build a Structured First-30-Days Protocol The first 30 days are where most onboarding plans fall apart. There's a week of orientation, a handshake introduction to the tech stack, and then the new advisor is largely on their own while senior staff attend to their existing books. A structured first-30-days protocol changes that. It specifies: What the new advisor shadows in week one: not generic observation, but specific client interactions with debrief time built in. What they own independently by week two: defined tasks with clear success criteria, not open-ended assignments. What the ops team sets up before day one: every access credential, every system login, every compliance filing, so the new advisor starts their first morning ready to work rather than waiting on IT. What the 30-day checkpoint looks like: a structured review that evaluates readiness against the playbook, not just a check-in conversation. The firms that do this well aren't just faster at onboarding. They retain new advisors at higher rates. When someone's first 30 days are structured and supported, they're more likely to feel competent and more likely to stay. That matters more than most firms realize: Cerulli Associates estimates that roughly 18,000 advisors changed firms in a recent year, a level of movement that reflects how often the employer-advisor relationship breaks down early. RIA onboarding best practices aren't just an ops concern. They're a direct lever on whether the advisors you recruit actually stay. Step Four: Connect Onboarding to Client Data Immediately One of the most damaging onboarding patterns is keeping new advisors away from client data until they're "ready." The instinct is understandable: you don't want mistakes. But it creates a longer productivity ramp and builds a culture of gatekeeping that's hard to unwind. The alternative is controlled access with guardrails. A new advisor should be able to view client portfolios, run planning scenarios, and generate draft proposals from day one, in a supervised or read-only capacity if needed, but with real data. That's how they learn the firm's methodology. That's how they develop judgment. The 2026 T3 survey noted that account aggregation tools now serve 52.81% of advisory firms, and the best implementations give advisors a complete picture of client holdings across custodians and held-away accounts. For a new advisor trying to understand a book of business, this isn't a nice-to-have. It's the difference between learning in real context versus learning in the abstract. Agentic AI amplifies this further. Rather than a new advisor manually pulling reports across systems, an agentic platform can surface the relevant client context automatically, prompt the advisor with the right next action, and log the interaction without any additional data entry. The advisor learns faster because the system is meeting them where they are, not the other way around. If your firm's onboarding protocol delays access to client data for more than a week, you're not protecting clients. You're slowing down your own advisor growth timeline. Step Five: Automate the Compliance Setup, Not Around It Compliance onboarding tends to be the last piece firms think about and the first thing that creates delays. State registrations, Form ADV updates, custodian credentialing, archiving setup, email monitoring activation: every one of these has dependencies and lead times. The solution isn't to rush compliance. It's to start it earlier and systematize it. Build a compliance checklist that begins the moment an offer is accepted, not the moment the advisor shows up. Work backward from the first day they need to be client-ready and map every compliance step to that date. Assign ownership to each step: not "ops will handle it," but a specific person with a specific deadline. This is another area where agentic AI is beginning to carry real weight. AI-driven compliance tools can monitor new advisor communications automatically, track required filings, flag issues in real time, and surface action items without manual review of every interaction. The 2026 T3 survey found compliance technology penetration at 30.15% of advisory firms, and the category is growing as firms realize that manual compliance review doesn't scale with headcount. For new advisors who are still learning what's permissible, an automated monitoring layer isn't surveillance. It's a safety net that protects both the advisor and the firm. Onboarding Is Now a Recruiting Argument There's a dimension to this that most ops teams underestimate. Advisors evaluating a move in 2026 are doing real diligence on the tech stack before they sign. They want to know what CRM the firm runs, whether workflows are documented, how long it typically takes a new advisor to get fully up to speed. The firms that can answer those questions clearly and confidently, with a playbook to show, have a material recruiting advantage over those that say "we'll figure it out once you're here." The promise of a smooth, well-structured onboarding experience is increasingly part of the offer itself. Cerulli Associates estimates roughly 18,000 advisors changed firms in a recent year. A meaningful portion of those moves were shaped not just by compensation or equity, but by the technology and operational environment the receiving firm could credibly demonstrate. An advisor who has experienced chaotic onboarding at a previous firm will weigh that heavily in their next decision. Firms that treat onboarding as an afterthought are not just slower to be productive. They're less competitive in recruiting. The two problems compound each other. What Scalable Onboarding Actually Looks Like? The firms that onboard advisors fastest share a few characteristics. They've built a playbook and maintain it: it's a living document that gets updated when the tech stack changes or when a new advisor surfaces a gap. They've reduced the number of systems a new advisor has to learn independently by choosing integrated platforms where possible. And they've made the ops team's role explicit: not to hand-hold advisors indefinitely, but to set up the conditions for independence as quickly as possible. Scale matters here. A firm that onboards two advisors a year can absorb a slow, informal process. A firm that's growing through acquisition or aggressive recruiting needs a repeatable system, one that produces the same output regardless of which ops person is running it or which advisor is going through it. The Agentic Wealth OS by OneVest is built around this kind of operational structure. When advisor workflows, client data, and compliance functions share a common agentic platform, onboarding isn't a manual process of provisioning access across seven different tools. It's a configuration, and configurations can be standardized, documented, and executed consistently. The agent works across the firm's systems so the new advisor doesn't have to. The 2026 Benchmark to Hold Yourself To If your new advisors are taking more than 60 days to run their first unsupervised client meeting, something in the onboarding process is broken. If they're still asking senior staff for help navigating the CRM after week four, the handoff was incomplete. If your ops team can't execute a new advisor setup in five business days, the process hasn't been systematized. These aren't aggressive standards. They're achievable ones, for firms that treat onboarding as an operational design problem rather than an orientation task. Advisor growth stalls when onboarding is slow. The revenue math is straightforward. The operational fix, if you've done the work to document and systematize it, is too. The firms that figure this out in 2026 will have a durable advantage in recruiting, retention, and growth, not because they have better advisors, but because they've built a better environment for advisors to succeed faster. Conclusion and Next Steps Scalable advisor onboarding doesn't happen by accident. It's the result of documented processes, integrated technology, and an ops team that treats the new hire's first 90 days as a system to be run, not a period to be survived. The firms getting this right are shortening their productivity ramp, improving retention, and building a repeatable foundation for growth. And increasingly, they're winning recruits before the conversation even gets to compensation. If you're ready to see what an agentic platform looks like in practice, explore the OneVest Agentic Wealth OS. Frequently Asked Questions: How long should it take to fully onboard a new advisor at an RIA? A well-structured onboarding process should have a new advisor running their first unsupervised client meeting within 60 days and operating independently within 90. If it's taking longer, the bottleneck is usually one of three things: fragmented tech access, undocumented processes, or delayed compliance setup. All three are fixable with the right systems in place. What's the biggest mistake RIAs make when onboarding new advisors? Treating onboarding as an orientation rather than an operational handoff. Most firms get the new hire set up with a laptop and a compliance walkthrough, then leave them to figure out the rest. The firms that onboard fastest have a written playbook, a pre-day-one checklist for ops, and a defined 30-day checkpoint. That structure is what separates a 45-day ramp from a 120-day one. How does advisor onboarding affect retention? Significantly. A new advisor who feels competent and supported in their first 30 days is far more likely to stay. When onboarding is disorganized, new hires often interpret the chaos as a signal about the firm itself. RIA onboarding best practices aren't just about productivity: they're a retention strategy, especially in a market where advisor movement is high and recruits are evaluating firms more carefully than ever before. Does the tech stack actually influence whether an advisor accepts an offer? Increasingly, yes. Advisors who have lived through a fragmented, poorly integrated tech environment at a previous firm treat the technology conversation as part of their diligence, not a detail to figure out later. A firm that can walk a recruit through a documented onboarding process and demonstrate a modern, connected platform is making a materially stronger offer than one that says "we'll get you set up once you start." Can agentic AI meaningfully improve advisor onboarding? Yes, in ways that go beyond simple automation. An agentic platform can surface client context at the right moment, prompt a new advisor on the next best action, route compliance tasks automatically, and handle meeting documentation without additional data entry. The result is that a new advisor operates closer to full productivity from day one, rather than spending the first 60 days learning how to find things. The 2026 T3 survey found AI notetaking tool adoption at 42.86% of advisory firms, and that's just one layer of what agentic AI can do across the full onboarding workflow. How do you onboard advisors faster without increasing compliance risk? Start the compliance setup the moment an offer is accepted, not on day one. Build a checklist with named owners and hard deadlines for every step: state registration, Form ADV updates, custodian credentialing, archiving activation. Agentic AI tools can monitor new advisor communications in real time and flag issues automatically, which means compliance oversight doesn't have to slow the ramp. Controlled access to client data with supervisor review is also a practical middle ground: new advisors learn in real context without the risk of unsupervised errors.

Blog

BlogAgentic AI vs. AI-Assisted Wealth Software: What's the Actual Difference?

The wealth management industry is using the word "AI" the way it once used "digital" as a signal of modernity rather than a description of what the technology actually does. Every CRM vendor, portfolio management platform, and compliance tool now claims to be AI-powered. Most of them are not lying. They are just describing something much narrower than what the term implies. The difference between AI-assisted and agentic wealth software is not a marketing distinction. It determines what your technology can actually do without someone managing it, and what it still cannot do without a human in the loop. For firms evaluating platforms or planning infrastructure investments in 2026, understanding that distinction is not optional. One clarification belongs at the front: agentic AI in wealth management is not about making financial decisions on behalf of clients. It does not execute trades, rebalance portfolios, or take any financially impactful action without human authorization. That boundary is non-negotiable, both from a compliance standpoint and from a fiduciary one. What agentic AI does is handle the operational and coordination work that surrounds those decisions: the follow-ups, the data pulls, the document reads, the workflow handoffs, the exception routing, and the audit trail. It removes the friction that slows firms down without touching the judgment that defines their value. What AI-Assisted Wealth Software Actually Does? AI-assisted tools are, broadly, software that uses machine learning or language models to make a human's work faster or better. The human is still the primary actor. The AI is a sophisticated assistant. In practice, this looks like a CRM that surfaces suggested next actions based on client activity patterns. It looks like a compliance tool that flags a document for review rather than requiring a coordinator to find it manually. It looks like a reporting system that generates a first draft of a client summary instead of requiring an advisor to write it from scratch. These capabilities are genuinely useful. They reduce time on repetitive tasks. They catch things that humans miss when moving quickly. They lower the cognitive load on operations staff managing large books of business. What they do not do is carry a workflow forward on their own. An AI-assisted tool surfaces the recommendation and may add intelligence to specific steps along the way, such as reading a document to extract key fields or scoring a risk flag. But progress through the workflow remains human-dependent. The follow-up to a flagged item, the exception that needs routing, the data connection that needs to be made, the next step that needs initiating: all of that still runs on human energy. The AI makes each individual touchpoint smarter. It does not reduce how many touchpoints the human has to manage. What Agentic AI Changes About That Model? Agentic AI shifts the architecture. Instead of a tool that assists a human through a process, an agentic system runs the process and surfaces only the exceptions that require human judgment. The distinction is not about AI being smarter. It is about autonomy across multi-step workflows. An agentic system does not stop after generating a recommendation. It initiates the next step, monitors completion, reads the incoming document to extract the data it needs, connects to the relevant system to verify the result, and flags the edge cases where automated action is not appropriate. In a wealth management context, this looks like a system that does not just identify a missing disclosure. It initiates the remediation workflow, reads the client file to confirm what version is on record, pulls the current regulatory requirement from the relevant source, tracks completion status, routes the unresolved item to the right reviewer on the right timeline, and maintains the audit trail. The compliance officer is not managing that process. They are reviewing a prioritized queue of items that actually need their attention. To be precise about scope: this system is not deciding whether to update that disclosure, not advising on the content of it, and not taking any client-facing action without authorization. It is doing the coordination and data work that surrounds the human decision, so that when the compliance officer sits down to review, everything they need is already assembled. The agentic AI use cases that matter most in this industry are not the ones that generate content or surface insights. They are the ones that close the gap between identifying a workflow item and completing it, without requiring a coordinator to manage each step in between. What Agentic AI Is Not Doing in Wealth Management? This point is worth its own section because the confusion is common and the stakes are high. Agentic AI in a wealth management platform does not make investment decisions. It does not execute trades. It does not rebalance portfolios or move client assets. It does not send client-facing communications without approval. It does not take any action that has financial or regulatory consequences without a human in the authorization chain. What it does do is the work that currently fills the hours of operations teams, advisors, and compliance staff before and after those decisions get made. It reads documents to pull the data a workflow needs rather than waiting for someone to do it manually. It connects to external systems through integrations to verify data without requiring a human to log in and check. It keeps workflows moving by following up on outstanding items, sending internal notifications, and surfacing what is blocked. It catches the step that would otherwise get missed when someone is managing fifteen other things simultaneously. The value is not in replacing judgment. It is in removing the coordination tax that judgment currently pays. The Technical Capabilities That Make It Work Two capabilities underpin what separates a genuinely agentic wealth platform from one that is simply AI-assisted with better marketing. The first is document reading and data extraction. An agentic system can read an uploaded document, a custodian statement, a compliance filing, or a client agreement and pull the relevant data points into the workflow without a human doing the extraction. This is not just optical character recognition. It is a contextual understanding of what a document contains, what fields matter for the current workflow, and what discrepancies exist between what the document says and what the system expects. The practical effect is that data entry errors decrease, processing time decreases, and the human reviewer receives a pre-analyzed file rather than a raw document. The second is connectivity across systems through MCP server integration. A siloed AI tool can process what is in front of it. An agentic platform connected to the firm's broader technology ecosystem can pull live data from a custodian, cross-reference it against a CRM record, check a compliance system for outstanding flags, and push a completed status update back to the workflow system. That connectivity is what allows an agentic system to act rather than just advise. Without it, even a sophisticated AI is still dependent on humans to move information between systems. Together, these capabilities mean the agentic system is operating with current, complete data rather than whatever happened to be loaded into it last. That matters for compliance accuracy. It matters for onboarding completeness. And it matters for the audit trail, which needs to reflect what actually happened, not what was manually entered after the fact. Why the Distinction Matters for Firm Operations? Most wealth management firms are not understaffed because they lack insight. They are understaffed because the operational workflows that keep a firm running, including onboarding, compliance monitoring, account servicing, and reporting, are built on manual coordination. People move information between systems. People follow up on incomplete items. People verify that the thing that was supposed to happen actually happened. AI-assisted tools make those people more efficient. Agentic systems change the ratio of people to workflows. This is where the operational case for agentic wealth software becomes concrete. A firm running fifty advisors with a five-person operations team is not limited by the intelligence of its tools. It is limited by how many workflows its operations team can actively manage. Add ten more advisors through an acquisition, and the firm does not need more intelligent tools. It needs tools that do not require the same per-unit coordination overhead. Agentic AI use cases in wealth management are largely about removing that per-unit ceiling. Compliance monitoring that scales to cover an expanded advisor population without proportional headcount. Onboarding workflows that run to completion without requiring an ops coordinator to track each step. Account servicing exceptions that are identified, routed, and resolved without someone managing the queue manually. And all of it happening without eliminating the compliance checkpoints and human authorization steps that the firm's supervisory program requires. Where AI-Assisted Tools Still Win? It would be wrong to frame this as AI-assisted tools being obsolete. They are not, and for many use cases they are the right answer. Tasks that are genuinely judgment-intensive, including constructing a financial plan, navigating a complex client conversation, and making portfolio allocation decisions, are not candidates for agentic automation. The value of AI assistance in those contexts is exactly the right framing: the technology augments human judgment without attempting to replace it. The same logic applies to novel situations. Agentic systems operate well within defined workflow boundaries. When a situation falls outside those boundaries, such as an unusual client request, a regulatory question with no clear precedent, or a compliance finding that requires senior review, the right response is to route it to a human, not to attempt autonomous resolution. A well-designed wealth AI platform does not try to automate everything. It automates what is appropriately automated and routes what is not. The sophistication is in knowing where that line is and building workflow architecture that respects it. The Practical Evaluation Question For a CTO or technology-forward advisor evaluating platforms, the distinction between AI-assisted and agentic wealth software translates into a set of concrete questions. When the system identifies an exception or a required action, what happens next? If the answer is "it alerts someone to take action," that is AI assistance. If the answer is "it initiates the next step in the workflow and alerts someone only when human judgment is required," that is agentic behavior. Can the system read documents and extract data into a workflow without manual input? Can it connect to external systems to pull live data rather than relying on what was last manually entered? These are the capabilities that separate operational automation from operational intelligence. How does the system handle multi-step processes? AI-assisted tools are typically single-step: they help with a discrete task. Agentic systems maintain state across a workflow. They know where a process is, what has been completed, and what needs to happen next without a human tracking it. Does the system scale without proportional coordination overhead? An AI-assisted tool scales with the humans using it. An agentic system scales with the volume of workflows it is managing. For firms growing through acquisition or advisor headcount, this is the practical question that determines whether the technology actually changes their operational capacity. What This Means for Platform Selection in 2026? The wealth AI conversation has moved past the question of whether AI belongs in wealth management. That debate is over. The question now is which category of AI capability a platform actually delivers and whether the answer matches what a firm's operational model actually requires. For firms at steady state with a stable advisor population and manageable workflow volume, AI-assisted tools may be exactly sufficient. The ROI is real. The efficiency gains are meaningful. For firms growing through acquisition, adding advisor headcount, or operating in a regulatory environment that demands complete supervisory documentation at scale, AI assistance is not enough. The coordination burden does not shrink as the firm grows. It compounds. The tools that help individuals work faster do not change the underlying ratio of people to workflows. Agentic wealth software exists to change that ratio. It does not remove judgment from the equation, and it does not touch the decisions that belong to advisors and compliance officers. It removes the coordination overhead that consumes the time and bandwidth that judgment requires. The firms evaluating technology through that lens, not feature breadth, not marketing language, but actual workflow autonomy, are the ones building infrastructure that will hold up as the operational surface area expands. Frequently Asked Questions: What is the main difference between AI-assisted and agentic wealth software? AI-assisted tools help humans work faster on individual tasks by surfacing recommendations, drafting content, or flagging exceptions. Agentic wealth software goes further: it carries the workflow forward, connects to external systems to pull live data, reads documents to extract what it needs, and routes only genuine exceptions to human reviewers. The human is still in the loop, but for judgment calls, not coordination. Does agentic AI make investment or trading decisions for clients? No, and this distinction matters. Agentic AI in a regulated wealth management context does not execute trades, rebalance portfolios, or take any financially impactful action without human authorization. Its role is operational: moving workflows forward, reading and processing documents, connecting to data sources, following up on outstanding items, and surfacing what needs human attention. The financial decisions remain with the advisor and the client. What are the most common agentic AI use cases in wealth management? The highest-impact use cases are operational: advisor onboarding workflows that run to completion without manual tracking, compliance monitoring that extends automatically to a growing advisor population, document reading and data extraction that eliminates manual entry errors, and account servicing exception management. These capabilities do not replace compliance checkpoints or human authorization steps. They handle the coordination work that surrounds them. How does document reading fit into an agentic wealth platform? Document reading allows the system to ingest a client agreement, custodian statement, or compliance filing and extract the relevant data into the workflow without requiring a human to do it manually. This reduces data entry errors, speeds up processing, and means the human reviewer receives a pre-analyzed file with discrepancies already flagged rather than a raw document to interpret from scratch. Is agentic AI a replacement for human advisors or compliance staff? No. Agentic systems handle defined, repeatable workflows, not judgment-intensive decisions. A well-built agentic platform routes novel situations, complex client needs, and regulatory edge cases to humans. The goal is to remove coordination overhead so that advisors and compliance professionals can focus on the work that actually requires their expertise. How does OneVest approach agentic AI in wealth management? OneVest's platform is built around agentic workflow automation across the core operational functions of a wealth management firm: onboarding, compliance monitoring, client account management, and servicing exceptions. The system reads documents to extract data, connects to external systems through MCP integrations to pull live information, maintains continuous oversight across advisor activity, routes exceptions for human review, and generates a complete audit trail, all without requiring manual coordination at each step. Financial decisions and client-facing actions remain with authorized humans. Learn more about OneVest's agentic AI capabilities. The Bottom Line The difference between AI-assisted and agentic wealth software is not a technical nuance. It is the difference between tools that make individuals more efficient and infrastructure that changes how many workflows a firm can manage without adding headcount. Neither category replaces the human judgment that wealth management is built on. The financial decisions, the compliance calls, the client relationships: those stay with the people whose names are on the license. What agentic software takes off their plate is the coordination tax: the follow-ups, the data pulls, the document reads, the exception routing, and the status tracking that currently consumes hours that should be spent on higher-value work. Both categories have a place. The question is whether the platform a firm is evaluating actually matches the operational demands it is trying to meet and whether the AI capabilities being marketed are the ones that will still hold up when the firm is twice its current size. Ready to see what agentic AI actually looks like inside a wealth management platform? Explore how OneVest helps firms move from coordination-heavy operations to scalable, agentic infrastructure.

Blog

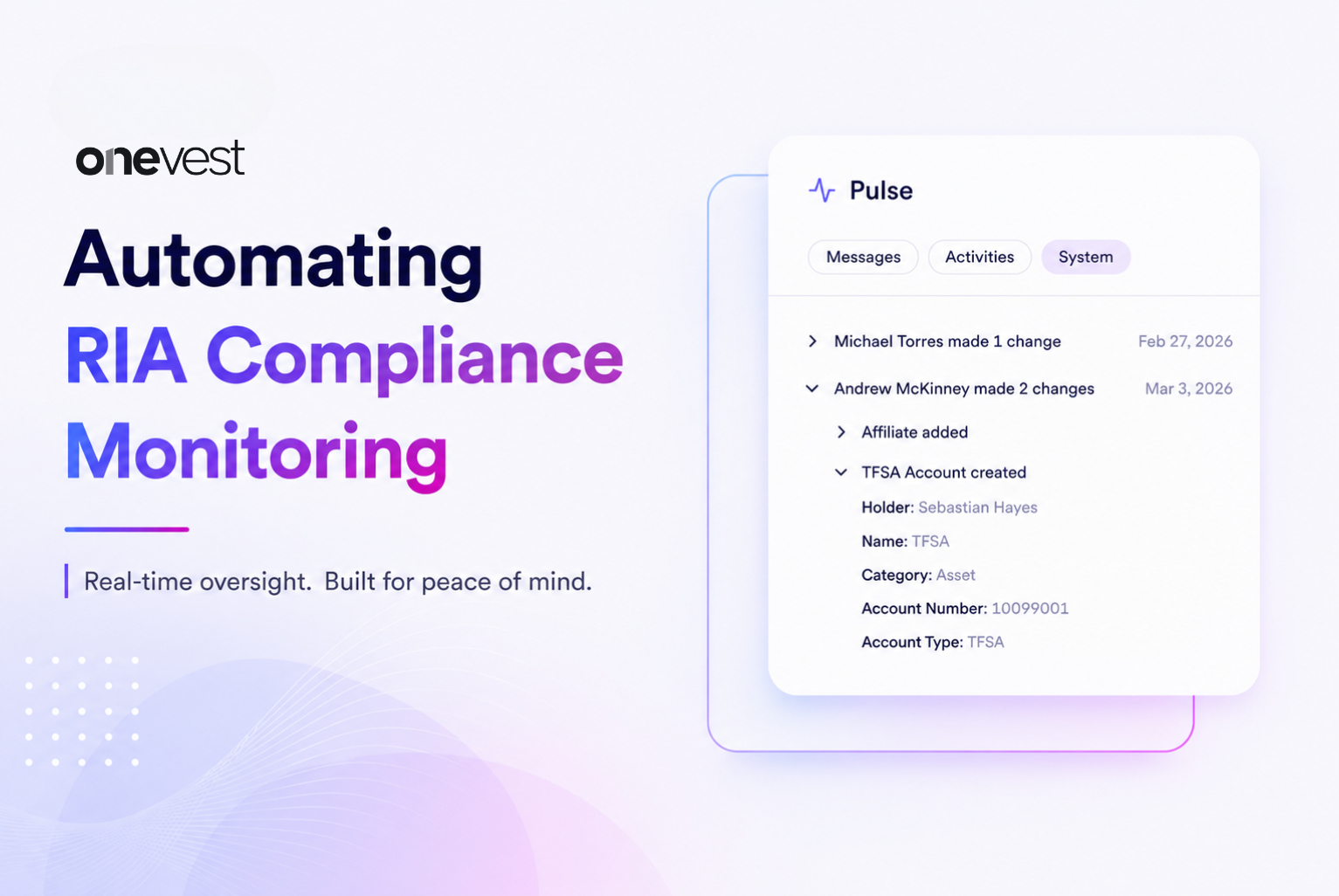

BlogAutomating RIA Compliance Monitoring: What Firms Need to Know in 2026

The SEC examination cycle is not getting quieter. In 2026, RIA compliance officers are managing more regulatory surface area, including heightened scrutiny of AI-driven investment tools, evolving cybersecurity disclosure requirements, and rising expectations around supervisory documentation, while the number of compliance staff at most firms has not kept pace. Something has to give. For a growing number of firms, what's giving way is the manual process model that has defined compliance monitoring for the past two decades. Automating RIA compliance monitoring is no longer a technology project for large enterprise firms with dedicated innovation teams. It is a practical necessity for any RIA that wants to manage compliance risk without building a larger headcount infrastructure to do it. Why Manual Compliance Monitoring Is a Structural Problem, Not a Staffing One? The standard response to compliance pressure has been to add staff. Hire another compliance analyst. Assign a dedicated reviewer to client communications. Build a checklist-heavy review process for account activity. This approach works until it doesn't, and in 2026, it is failing at scale. The problem is not that compliance teams lack skill or diligence. The problem is that the volume of touchpoints that require monitoring has grown faster than any team can absorb manually. A mid-sized RIA managing 500 client relationships generates continuous compliance-relevant activity: account changes, fee disclosures, client communication, third-party data integrations, and more. Tracking all of it through spreadsheets, periodic audits, and after-the-fact reviews creates gaps, and those gaps are exactly where examination findings live. Manual monitoring is also inherently reactive. By the time a supervisory review surfaces an issue, the violation has already occurred. Remediation takes longer than prevention, and regulators treat pattern failures more seriously than isolated incidents. According to the SEC's 2024 examination priorities report, deficiencies in compliance programs and supervisory procedures remain among the most frequently cited findings across registered investment advisers. Firms that continue to treat compliance monitoring as a headcount problem will keep hiring into a structural gap. The answer is infrastructure, not personnel. What Automating RIA Compliance Monitoring Actually Means? "Automated compliance" is a phrase that gets applied loosely. It is worth being precise about what it means in practice, because the distinction between basic rule-based alerts and genuinely intelligent compliance infrastructure is significant. Rule-based compliance tools run conditional logic against structured data. If a trade exceeds a size threshold, flag it. If a client document is missing a field, block submission. These tools reduce obvious errors, and most firms have some version of them already. What they cannot do is monitor the full operational lifecycle of a client relationship across systems, surface patterns that suggest emerging risk, or adapt to regulatory changes without manual reconfiguration. Modern automated compliance monitoring does all of that. It connects to the firm's data infrastructure, including CRM, portfolio management, custodian feeds, and communication logs, and monitors activity continuously. It applies rules that can be updated centrally as guidance evolves. It generates exception reports that direct compliance staff to the issues that require human judgment, rather than requiring them to manually search for problems across siloed systems. The practical effect: compliance officers spend less time collecting data and more time acting on it. How Agentic AI Changes the Compliance Monitoring Model? Agentic AI takes automation a meaningful step further. Where traditional compliance tools wait for a rule to be triggered, agentic systems actively work through multi-step monitoring processes. They gather data across systems, cross-reference it against policy requirements, identify patterns that warrant attention, and surface prioritized findings for review. They do not wait to be asked. They move through the work continuously and bring the right issues forward. In practice, this looks like an intelligent layer that reconciles trade activity against client suitability profiles, tracks document and disclosure status across the full client base, monitors account servicing activity for exceptions, and flags issues with context, all without a compliance analyst having to manually pull and compare data across platforms. What agentic AI does not do is make compliance determinations. That distinction matters enormously. The system's role is to do the investigative legwork: identify the anomaly, assemble the relevant context, and route it to the right person with enough information to make a sound judgment quickly. The compliance officer or principal remains the decision-maker. Every finding the system surfaces is a prompt for human review, not a conclusion. This is the correct model, not just from a regulatory standpoint where human supervisory accountability is a non-negotiable requirement, but from a practical one. Compliance decisions involve nuance, client context, and professional judgment that no automated system should be substituting for. The value of agentic AI is that it makes the human decision-maker faster, better-informed, and less likely to miss something. It does not remove them from the loop. The Key Gaps That Supervisory Tools Close For compliance officers, the value of automated supervisory tools is most visible in four areas where manual processes consistently fall short. Trade and fee monitoring: Regulation Best Interest obligations require ongoing documentation that investment recommendations are in the client's best interest. Automated monitoring can cross-reference trade activity against client profiles, flag potential outliers, and generate the documentation trail that supports supervisory sign-off in real time rather than at the end of the quarter. Document and disclosure tracking: Missing disclosures, stale Form ADV language, and unsigned acknowledgments are perennial exam findings. An automated system tracks document status across all client accounts and surfaces gaps before they become deficiencies, not after. Account servicing oversight: Changes to account details, money movement requests, and administrative updates all carry compliance implications. Automated workflows log every action, flag exceptions that fall outside defined parameters, and create a clean record for supervisory review without requiring a coordinator to manually track each transaction. Third-party and vendor oversight: RIAs increasingly rely on third-party technology providers and model portfolio vendors, which creates compliance obligations around due diligence, data security, and conflicts of interest. Automated workflows can maintain a live inventory of vendor relationships and trigger periodic review requirements without relying on a compliance team member to remember to do it. The Regulatory Landscape Driving Urgency Right Now Several intersecting regulatory developments make 2026 a particularly important moment to assess compliance infrastructure. AI adoption across wealth management has added a new compliance dimension. Firms using AI-assisted investment tools, client communication platforms, or data analytics services face expectations around explainability, oversight, and documentation of how those tools influence client outcomes. Manual compliance processes were not designed for this level of operational complexity. Cybersecurity rules have expanded the compliance perimeter further. The SEC's cybersecurity disclosure requirements demand documented policies, tested procedures, and timely reporting of material incidents, all of which require operational infrastructure, not just written protocols. Regulation Best Interest continues to generate examination activity. Firms need to demonstrate ongoing, documented processes for evaluating whether recommendations serve client interests, not one-time policy adoption. That documentation burden falls directly on compliance and operations teams and is difficult to sustain at scale without automated record-keeping and monitoring. Taken together, these regulatory developments are adding compliance monitoring requirements that will not be absorbed by current staffing models without something changing in how the work gets done. Building the Internal Case for Compliance Automation Compliance officers and RIA principals who understand the operational need often face a harder challenge internally: making the case for investment when the cost of compliance failure is invisible until it isn't. The argument is strongest when framed around three quantifiable risks. The first is examination readiness. Firms that cannot produce clean, organized documentation of supervisory activity during an SEC exam face findings that consume significant time and legal resources to remediate. Automated systems generate that documentation as a byproduct of normal operations. The second is the cost of manual labor applied to low-judgment tasks. A compliance analyst spending 40 percent of their time pulling data from disparate systems, reconciling records, and building status reports is not doing compliance work. They are doing data work. Automation redirects that capacity toward the analysis and judgment that compliance professionals are actually hired to provide. The third is the risk of scaling without scaling compliance infrastructure. Every advisor added, every new custodian relationship, every expanded service offering increases the compliance surface area. If monitoring capacity does not scale with the firm, risk accumulates silently until an examination or incident surfaces it. What Implementation Actually Looks Like? Deloitte’s industry data suggests that firms implementing structured compliance automation reduce the time spent on manual monitoring tasks by 40 to 60 percent within the first year, with the largest gains in document tracking and trade surveillance. A survey by the Investment Adviser Association found that 74 percent of RIAs cited technology investment as a top priority for improving compliance program effectiveness, yet fewer than a third described their current tools as fully integrated. The steps below reflect a practical, staged approach that builds confidence without requiring a full systems overhaul. Step 1: Operational Audit. Map every manual compliance workflow. Identify where data is pulled from, who reviews what, and where handoffs between systems and people occur. Step 2: Define Scaling Objectives. Set specific targets for examination readiness, supervisory coverage ratios, and documentation standards. These targets guide system configuration. Step 3: Prioritize High-Volume, Low-Judgment Workflows. Start with document status tracking, trade monitoring, and account servicing exceptions. These deliver the fastest reduction in compliance risk and staff burden. Step 4: Configure Human-in-the-Loop Oversight. Define precisely what the system escalates and who reviews it. Automation surfaces exceptions. Compliance officers make the calls. Step 5: Build Audit Trail Architecture. Design for auditability from day one. The documented evidence of supervisory activity is what protects firms in examinations, not the automation itself. Step 6: Establish a Governance Cadence. Assign ownership for maintaining rule logic, reviewing exception rates, and incorporating regulatory changes. Automation reduces ongoing labor but does not eliminate governance responsibility. Step 7: Measure, Iterate, and Expand. Track supervisory coverage, exception volumes, and staff time recaptured. Use data to guide expansion into more complex compliance functions and to build the ongoing case for investment. The Stakes for Firms That Wait Compliance infrastructure investment has a compounding return. Firms that automate their supervisory workflows now are not just reducing today's risk. They are building a documented supervisory history that serves them in every future examination and a monitoring capacity that scales with growth without proportional headcount increases. The firms waiting for the compliance landscape to stabilize before making this investment are likely waiting for a moment that will not come. Regulatory expectations for documentation, surveillance, and oversight will not decrease. The operational complexity of managing client relationships across modern wealth management infrastructure will not decrease. The pressure on compliance staff to do more with flat or limited resources will not decrease. Automating RIA compliance monitoring is how compliance officers stop managing compliance risk reactively and start getting ahead of it. The infrastructure exists. The regulatory pressure is real. The case for action in 2026 is clear. Frequently Asked Questions: How does agentic AI differ from the compliance software many RIAs already use? Most existing compliance tools are reactive. They flag a problem after a rule is broken or require a person to manually run a report to check for issues. Agentic systems are proactive. They continuously work through multi-step monitoring processes across systems, surfacing prioritized exceptions for human review rather than waiting to be queried. The practical difference is that compliance officers are managing a curated queue of issues that need judgment rather than spending their time collecting data to find out whether issues exist. Can a firm implement compliance automation without replacing its existing technology stack? In most cases, yes. Modern compliance automation platforms are designed to integrate with existing CRM, portfolio management, and custodian infrastructure rather than replace it. The starting point is an operational audit that maps current workflows and identifies where manual steps can be automated within the existing environment. Full system replacement is rarely required and rarely the right first step. What should a compliance officer look for when evaluating automated supervisory tools? The most important criteria are integration depth, auditability, and configurability. The tool needs to connect to the systems where compliance-relevant activity actually occurs, generate a retrievable audit trail of every action taken, and allow compliance staff to configure escalation rules as regulatory guidance evolves. Firms should also evaluate the vendor's track record with SEC examination support and their approach to regulatory change management. How do you maintain human oversight when compliance workflows are largely automated? The key is designing escalation into the system from the start, not bolting it on afterward. Every automated workflow should have defined points where the system routes a finding to a compliance officer or principal for review and sign-off. High-stakes actions, including final account approvals, large fund movements, and exception handling, should require human validation before execution. The compliance officer's role shifts from manually hunting for problems to reviewing a prioritized queue of issues the system has already identified and contextualized. How does OneVest support compliance monitoring within its platform? OneVest provides integrated supervision powered by agentic AI, built directly into the operational workflows of the platform rather than sitting alongside them as a separate tool. The system continuously monitors activity across onboarding, account servicing, money movement, and client data, surfacing exceptions and routing them to the appropriate compliance reviewer with the context needed to make a fast, informed decision. Every action is logged automatically, creating a complete and retrievable audit trail without additional manual documentation effort. Compliance determinations remain with the firm's own principals and compliance officers. OneVest's role is to make sure nothing is missed and that every decision is supported by clean, organized, exam-ready documentation. Conclusion and Next Steps Automating RIA compliance monitoring is not a trend to watch from a distance. It is the operational standard defining competitive advantage in 2026, particularly for RIA firms managing growing advisor teams, expanding client bases, and increasing regulatory surface area. The firms that are staying ahead of compliance risk right now are not necessarily the ones with the largest compliance teams. They are the ones that have built intelligent supervisory infrastructure underneath their compliance officers, infrastructure that continuously monitors, surfaces, and documents issues without requiring a person to manually coordinate every step. Every advisor a firm adds, every new custodian relationship it opens, every acquisition it integrates increases the compliance workload. That workload becomes manageable when the firm is operating on infrastructure designed to scale with it. Without that infrastructure, each expansion creates new exposure. The gap between firms that have made this investment and those that have not will only widen as regulatory expectations continue to rise through 2027 and beyond. The next step for any compliance officer or RIA principal is practical. Audit your current supervisory workflows, identify where manual processes are creating gaps or delays, and evaluate whether your current technology can support the oversight obligations that come with the firm you are building toward. Intelligent compliance infrastructure is not about replacing the judgment that makes your compliance program effective. It is about giving that judgment the operational support it needs to work at scale. Ready to modernize your firm's compliance infrastructure? Join leading RIA firms already using OneVest to build supervisory workflows that scale without scaling headcount. Explore OneVest.